Indonesia Accelerates Bauxite-to-Aluminium Downstream Processing, Creating 15 Times More Value

23 Jul 2026, 10:55 AM

144

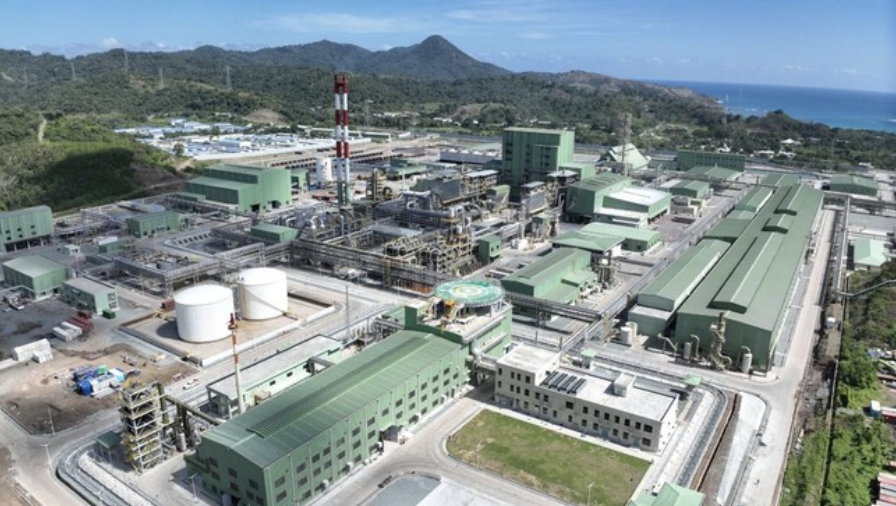

The Indonesian Bauxite Association (ABI) says accelerating downstream processing of bauxite through to aluminium production could increase the commodity's value by as much as 10 to 15 times."If bauxite is sold as raw ore, its value is very low. However, once it is fully processed, its value can increase by 10 to 15 times, depending on quality and market prices," ABI Chairman Ronald Sulistyanto told Bisnis on Thursday (23 July 2026).Ronald added that fully processing bauxite into aluminium is crucial to reducing Indonesia's reliance on imports.Indonesia's domestic aluminium demand is still largely met through imports, as locally produced alumina has yet to be processed further into aluminium on a significant scale."Particularly for aluminium, most of our domestic demand has long been met through imports because the alumina we produce is not yet processed further. If we process it all the way into aluminium, the economic value generated will be substantial," he said.Investment ShiftHe said investment is now shifting simultaneously from bauxite refining into alumina production and further downstream into aluminium smelting.Since the government launched its downstream processing policy in 2014, Ronald said Indonesia's bauxite mining industry has continued to record positive developments, particularly with the entry of new investors."Over the past three to four years, the development of aluminium smelters in Indonesia has accelerated significantly," he said.According to ABI, around 17 companies are currently involved in bauxite-to-alumina processing projects. Of these, 14 are in the preparation stage, while three have already broken ground.In the aluminium refining segment, ABI estimates that three to four companies have begun constructing aluminium smelters, while another five are in the planning phase."We are very pleased to see the optimism surrounding bauxite downstream processing finally becoming a reality," Ronald said.Maintain Production BalanceDespite rising downstream investment, Ronald believes Indonesia should maintain annual bauxite ore production at around 50 million tonnes."Production should not exceed around 50 million tonnes per year. In addition to preserving reserves, this is important to keep bauxite ore prices at healthy levels," he said.According to Ronald, annual bauxite production of around 50 million tonnes would generate an estimated 15 million to 17 million tonnes of alumina.Assuming each refinery produces around 2 million tonnes of alumina annually, Indonesia would require a maximum of about eight refineries.If each refinery has a capacity of 3 million tonnes per year, the country would need only around five to six facilities."This is a simple estimate based on the material balance between bauxite ore production and alumina requirements," he said.He added that maintaining this balance is essential to ensuring refinery investments remain economically viable throughout their operational lifespan.For the first time, domestic bauxite downstream projects have become Indonesia's largest source of downstream investment, overtaking nickel, which has long dominated investment in the mineral processing sector.According to data from the Ministry of Investment and Downstream Processing/Investment Coordinating Board (BKPM), the bauxite sector became the main driver of national investment growth in the second quarter of 2026, recording realised investment of IDR 40.1 trillion.The figure represents a 193% increase from IDR 13.7 trillion in the first quarter of 2026.Bauxite was followed by nickel with IDR 29.4 trillion in realised investment, copper at IDR 16.7 trillion, steel at IDR 13.2 trillion, silica sand at IDR 4 trillion, and other commodities—including tin, gold, silver, cobalt, manganese, coal, Buton asphalt, and rare earth metals—totalling IDR 4.7 trillion.Minister of Investment and Downstream Processing and BKPM Head Rosan Perkasa Roeslani said the shift was driven by the accelerated development of bauxite processing projects financed by both domestic and foreign investors."Bauxite is now number one. Usually nickel takes the top spot, but we are seeing a shift because several bauxite processing projects are being developed by both domestic and foreign investors," Rosan said while presenting Indonesia's investment performance to President Prabowo Subianto at the Presidential Palace complex recently.According to Rosan, the trend demonstrates that Indonesia's downstream processing programme is no longer dependent on a single natural resource.However, he acknowledged that processing for most non-nickel commodities remains in the early stages of supply chain development."The downstream processing we are undertaking for many commodities is still largely at the first or second stage," he said.