Amman Mineral (AMMN) Smelter Performance Improves

15 Aug 2025, 10:29 AM

5927

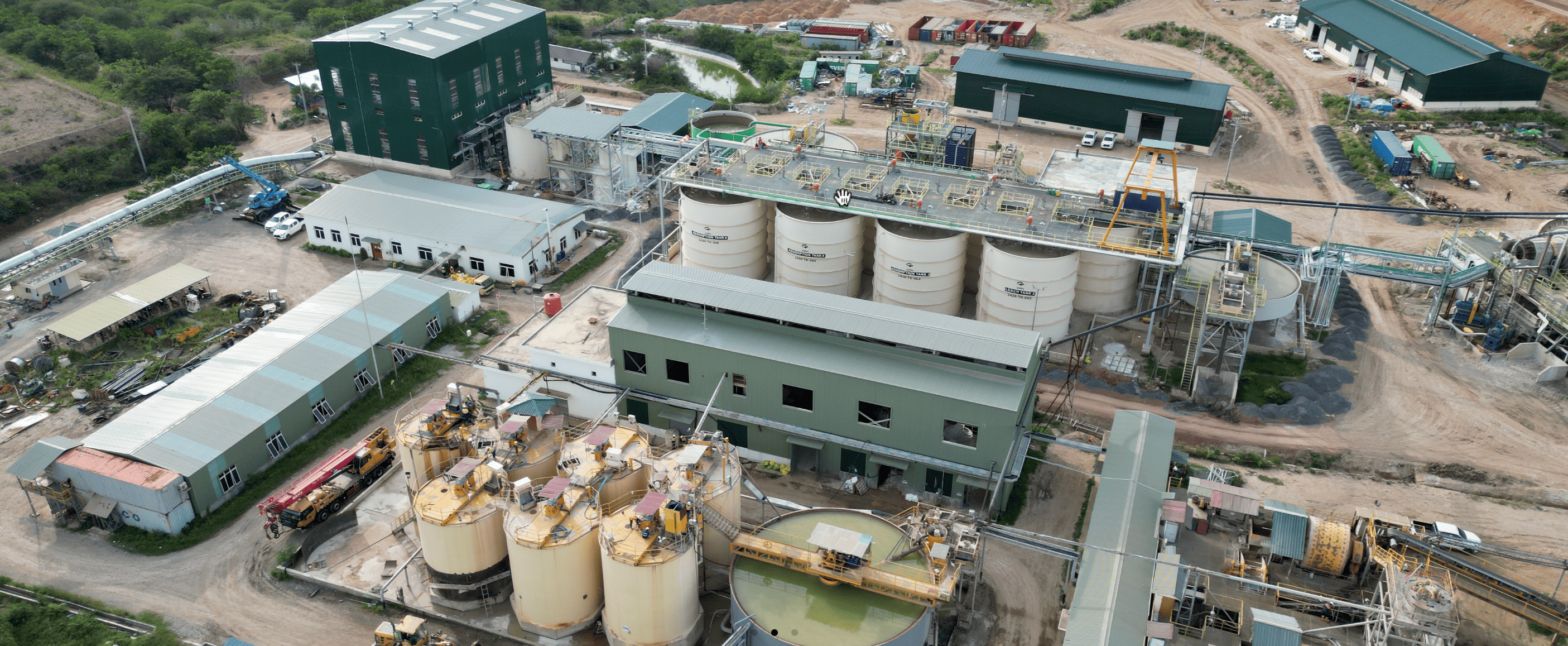

PT Amman Mineral Internasional Tbk (AMMN) has the potential to deliver positive performance in the second half of this year. This is in line with improved smelter performance following the initial commissioning phase, or comprehensive testing and inspection conducted by the issuer.AMMN President Director Arief Sidarto stated that the AMMN copper smelter successfully produced 19,805 tons, or 44 million pounds, of copper cathode. This production jumped from 635 tons in the first quarter of 2025 to 19,170 tons, as the smelter's performance improved following the initial commissioning phase. Average cathode production during the second quarter of 2025 reached 35% of total capacity.Arief said that production volume is projected to continue to increase in line with ongoing improvements to smelter operations."In mid-July, we reached another important milestone with the successful production of the first pure gold from our PMR facility," Arief said in a press release on Thursday (31/7/2025).However, Arief acknowledged that AMMN is facing operational challenges, particularly the transition to full production, due to the complex and time-consuming process. Therefore, AMMN is actively discussing with the government regarding the re-obtaining of its concentrate export permit.As is known, the government banned the export of this commodity earlier this year. This forced AMMN's sales to shift to copper cathodes starting in April 2025, which subsequently impacted the sluggish first-half performance results, as they were only based on second-quarter 2025 data. During the first half of 2025, AMMN recorded net sales of USD 183 million, largely driven by copper cathode sales in the second quarter of 2025. However, this figure was significantly lower than the company's net sales of USD 1.53 billion in the first half of 2024.Despite this, AMMN's EBITDA in the first half of 2025 reached USD 86 million, a significant improvement from the negative EBITDA of USD 42 million in the first quarter of 2025. This increase was primarily driven by stronger operational performance in the second quarter of 2025, when the company recorded positive EBITDA of USD 128 million.AMMN's net loss also decreased significantly from USD 138 million in the first quarter of 2025 to USD 8 million in the second quarter of 2025, resulting in a total net loss of USD 146 million at the end of the first semester of 2025.Arief added that overburden removal from Batu Hijau Phase 8 mining activities is currently progressing from the upper bench to the bottom of the pit, and is expected to reach the bottom of the pit in 2026 or 2027. AMMN can now access large quantities of fresh ore.As of the second quarter of 2025, mining volume has increased significantly from 1 million tons to 5 million tons."Mining activities are expected to still achieve annual production targets," he said.Nafan Aji Gusta, Senior Market Analyst at Mirae Asset Sekuritas, said the increase in smelter operations is projected to increase revenue, thereby reducing AMMN's losses this year.This also aligns with the 0% tariff on copper exports to the United States, a result of a recent trade agreement. "AMMN should be able to leverage this to maximize exports of processed copper products to the US," Nafan explained.In addition, another positive sentiment that could boost AMMN's performance is the potential for rising copper prices in line with the global economic recovery, particularly to meet cable manufacturing needs."Moreover, global demand for cables is increasing for both land and sea connectivity," he explained.

Korea Investment and Securities Indonesia (KISI) analyst Muhammad Wafi assessed that although there are opportunities for improvement, challenges will remain, such as high costs or suboptimal revenue."But there's potential for better results because construction progress is already over 90% and operations will begin at the end of the year," he said.Although the 0% tariff on copper products has come into effect, Wafi estimates that its impact will only be felt in 2026 because it will take time for smelters to be fully operational and produce significant export volumes.Looking ahead, the positive sentiment that will boost AMMN's performance is the prospect of rising copper prices in line with the global energy transition, which requires significant copper demand, such as in electric cars and renewable energy.But in the short term, there are risks of high loan interest costs, the risk of smelter delays, and copper price volatility.Wafi recommends holding AMMN shares, with a target price of IDR 8,000 per share.Meanwhile, Nafan recommends accumulative buying with a target price of IDR 8,850.On the other hand, technically, MNC Sekuritas analyst Herditya Wicaksana sees AMMN's movement still in an uptrend in the short term, but today's movement is accompanied by the emergence of selling pressure.He stated that the MACD and Stochastic indicators are trending downward, but he warned of potential corrections. Therefore, he recommended a buy trade with support at IDR 8,300 and resistance at IDR 8,700. His price target is in the range of IDR 8,850-IDR 9,000.